The Bottom Up Beta Calculator is a financial tool used to estimate the systematic risk of a company’s stock. Bottom-up beta reflects the risk of a company’s equity by factoring in the specific risks related to its industry and capital structure. It is derived from the unlevered beta of comparable companies and adjusted for the company’s leverage, i.e., the proportion of debt to equity. This method offers a more tailored estimate of risk than simply using the historical beta, which may not always be reflective of the company’s future risk profile.

Bottom-up beta is widely used in valuation, particularly in discounted cash flow (DCF) analysis, to estimate the cost of equity for a company. By understanding the risk relative to the overall market, investors can make better-informed decisions about the expected return on investment.

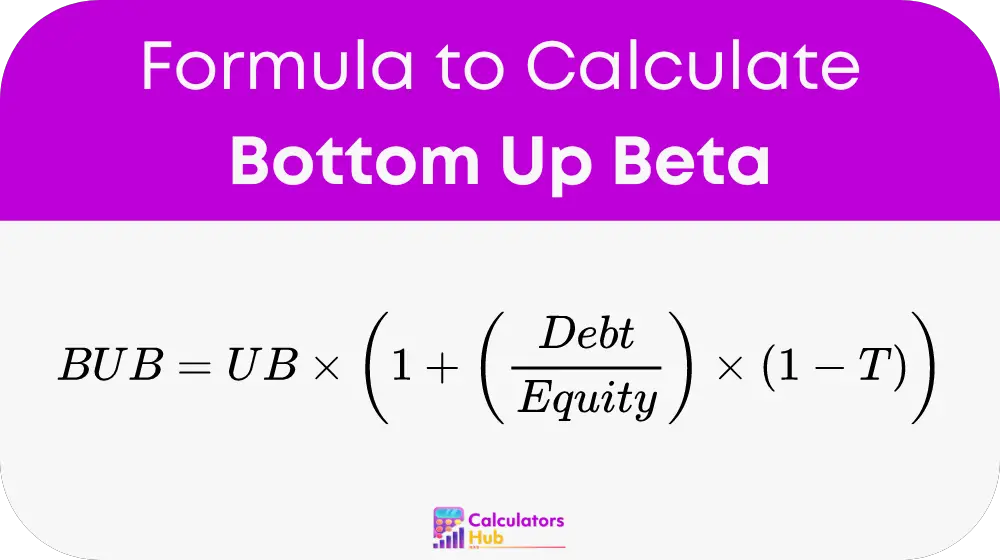

Formula of Bottom Up Beta Calculator

The formula for calculating bottom-up beta is:

Variables:

- BUB: Bottom-Up Beta, the estimated beta after adjusting for the company’s leverage (debt).

- UB: Unlevered Beta, which reflects the company’s risk without considering its debt. It is often derived from industry averages.

- D: Total Debt, the total amount of debt a company has.

- E: Total Equity, the total amount of shareholder equity.

- T: Tax Rate, typically expressed as a decimal (e.g., 0.30 for a 30% tax rate). The tax shield on debt is accounted for in this formula.

Key Points:

- Unlevered Beta (UB) is the beta of the company without considering its financial structure (debt), offering a measure of its operational risk.

- Debt (D) to Equity (E) ratio is use to adjust for leverage, as companies with more debt are typically riskier and have a higher beta.

- Tax Rate (T) is include because interest on debt is tax-deductible, reducing the overall cost of debt and thus affecting the beta calculation.

Common Terms and Reference Table

Here’s a table that outlines common terms and their definitions, making it easier for users to understand and apply the Bottom Up Beta Calculator:

| Term | Definition |

|---|---|

| Unlevered Beta (UB) | A measure of a company’s risk without considering its debt, typically based on industry averages. |

| Debt (D) | The total amount of a company’s debt, including both short-term and long-term liabilities. |

| Equity (E) | The total value of a company’s equity, representing ownership interest. |

| Debt-to-Equity Ratio | The proportion of debt relative to equity, used to adjust the company’s risk profile. |

| Tax Rate (T) | The percentage of a company’s earnings paid in taxes, affecting how much debt influences risk. |

This table provides a quick reference for understanding key factors in calculating bottom-up beta.

Example of Bottom Up Beta Calculator

Let’s go through an example to demonstrate how the Bottom Up Beta Calculator works.

Assume a company has the following financial data:

- Unlevered Beta (UB): 0.80 (derived from industry peers)

- Debt (D): $1,000,000

- Equity (E): $3,000,000

- Tax Rate (T): 30% (or 0.30)

Step 1: Apply the Formula

Bottom-Up Beta (BUB) = (Unlevered Beta (UB) × (1 + ((Debt (D) ÷ Equity (E)) × (1 – Tax Rate (T)))))

Substitute the values:

BUB = (0.80 × (1 + (($1,000,000 ÷ $3,000,000) × (1 – 0.30))))

Step 2: Calculate

BUB = (0.80 × (1 + (0.3333 × 0.70))) BUB = (0.80 × (1 + 0.2333)) BUB = (0.80 × 1.2333) BUB = 0.9866

The company’s bottom-up beta is approximately 0.99. This means the company’s risk is almost in line with the market average, with a slightly lower systematic risk.

Most Common FAQs

Bottom-up beta is prefer because it is forward-looking and based on industry and capital structure data, while historical beta relies solely on past stock performance, which may not accurately reflect the company’s current or future risk profile. It provides a more customized risk estimate by factoring in the company’s debt level and specific industry risks.

The debt-to-equity ratio directly influences bottom-up beta by adjusting for financial leverage. A higher ratio means the company is more reliant on debt, increasing its risk and thus raising its beta. Conversely, a lower ratio indicates less financial risk and results in a lower beta.

Yes, bottom-up beta is particularly useful for new or private companies with limited historical stock data. It relies on industry averages for unlevered beta and adjusts for the company’s specific debt and equity structure, making it a valuable tool for startups or companies without a long track record.