The Annual Forward Premium Calculator is a vital tool in the foreign exchange market. It helps investors, traders, and financial analysts measure the expected movement in exchange rates over a specific period. This tool is crucial for making informed decisions regarding currency investments, hedging strategies, and risk management in international trade.

Formula of Annual Forward Premium Calculator

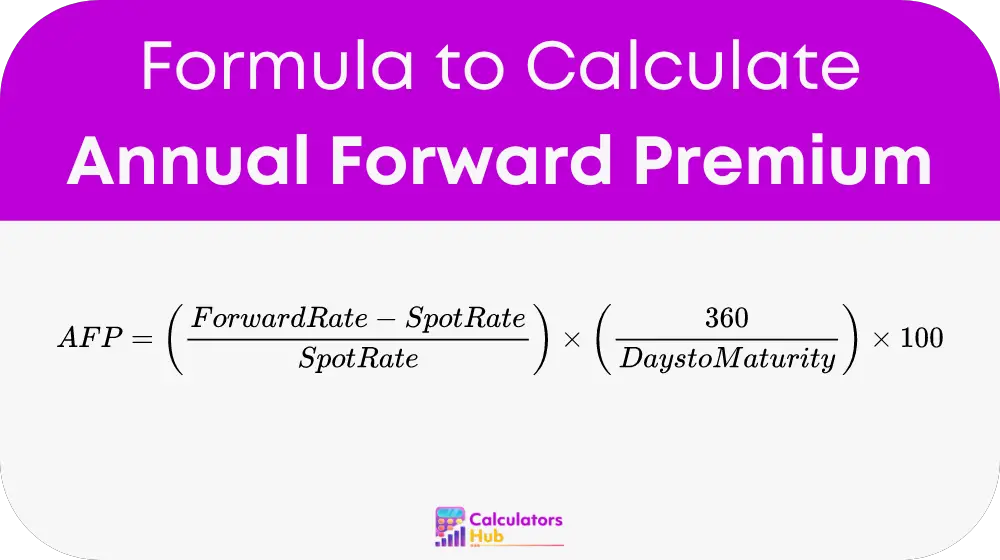

The Annual Forward Premium (AFP) is calculated using the following formula, which offers a clear view of the future expectations in currency value changes:

Where:

- Forward Rate: The agreed-upon exchange rate for a currency pair at a future date.

- Spot Rate: The current exchange rate for the currency pair.

- Days to Maturity: The number of days until the forward contract expires.

- 360: The standard number of days used in financial calculations for a year (adjust to 365 if required by specific market context).

Table of General Terms

This table provides a quick reference for commonly searched terms related to the Annual Forward Premium, aiding users in understanding without deep diving into calculations each time:

| Term | Definition |

|---|---|

| Forward Rate | The rate agreed upon for exchanging currency at a future date. |

| Spot Rate | The current rate at which a currency can be exchanged. |

| Days to Maturity | The duration until the forward contract's obligation must be fulfilled. |

| Annual Forward Premium | The expected percentage difference between the forward and spot rates, annualized. |

Example of Annual Forward Premium Calculator

Consider a scenario where the forward rate for USD/EUR in three months is 1.10 while the current spot rate is 1.08. Using the AFP formula:

AFP = [(1.10 - 1.08) / 1.08] * (360 / 90) * 100 = 8.33%

This calculation indicates an 8.33% annualized premium, suggesting expectations of a stronger EUR against the USD over the next three months.

Most Common FAQs

It provides insights into market expectations about currency movements, influencing trading strategies and risk management.

Using 360 days simplifies the calculation and aligns with banking standards, while 365 days gives a slightly more precise measure based on actual days in a year.

Yes, a negative AFP suggests that the forward rate is lower than the spot rate, indicating expected depreciation of the currency.