A Forward Rate Calculator is a financial tool that determines the interest rate for a loan or investment that is expected to start at a future date. It does not predict the future; instead, it calculates the "implied" rate that is consistent with today's interest rates for various time periods (known as spot rates). By comparing the interest rate for a long-term investment with a short-term investment, the calculator deduces the rate that must apply in the future period to make both options financially equivalent. Consequently, investors, financial analysts, and corporate treasurers use this calculation to understand market expectations, hedge against interest rate changes, and price financial derivatives.

class="wp-block-heading">formula of Forward Rate Calculator

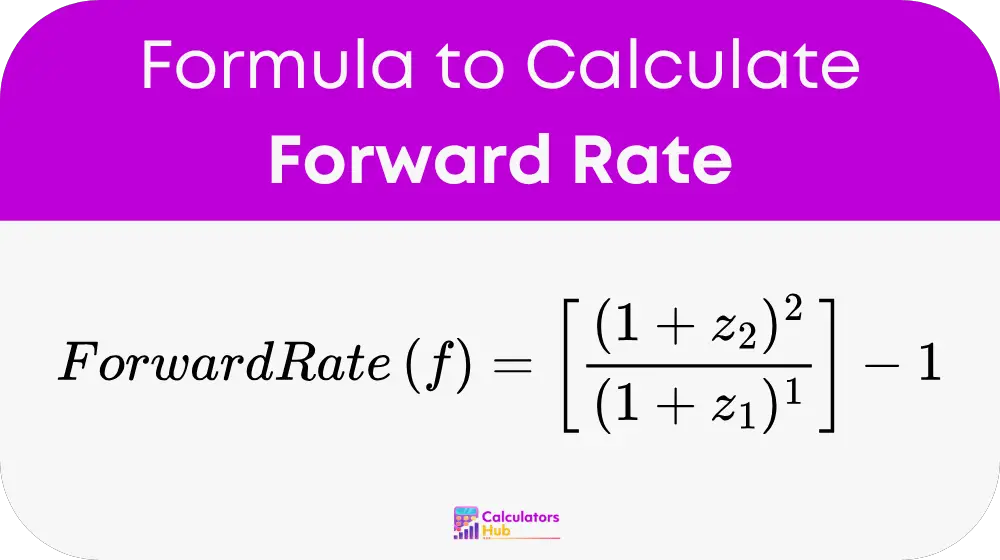

The forward interest rate can be found by using the current spot rates for two different time periods.

Where:

f = The implied forward rate for the period between the end of the first term and the end of the second term.

z₁ = The current spot interest rate for the first period (e.g., one year), expressed as a decimal.

z₂ = The current spot interest rate for the entire second period (e.g., two years), expressed as a decimal.

T

he exponents (1 and 2) represent the length of the respective periods in years. This formula can be generalized for different time frames.Implied Forward Rates Based on Yield Curve Shape

The shape of the current yield curve (the relationship between spot rates and maturity) strongly influences the implied forward rate. This table shows what different yield curve shapes suggest about market expectations for future interest rates.

| Yield Curve Shape | Spot Rate Example | Implied Forward Rate | Market Interpretation |

| Normal (Upward) | 1-Year = 3%, 2-Year = 4% | Higher than both spot rates. | The market expects interest rates to rise in the future. |

| Flat | 1-Year = 3%, 2-Year = 3% | Equal to the spot rates. | The market expects interest rates to remain stable. |

| Inverted (Downward) | 1-Year = 4%, 2-Year = 3% | Lower than both spot rates. | The market expects interest rates to fall in the future. |

Example of Forward Rate Calculator

Let's calculate the one-year forward rate that is expected to start one year from today.

First, we gather the current spot rates from the market.

-

class="wp-block-list">

- The spot rate for a 1-year investment (z₁) is 3% or 0.03.

- The spot rate for a 2-year investment (z₂) is 4% or 0.04.

Next, we plug these values into the forward rate formula.

Forward Rate (f) = [(1 + z₂)² / (1 + z₁)¹] − 1

Forward Rate (f) = [(1.04)² / 1.03] − 1 = 0.050097

To express this as a percentage, we multiply by 100.

Forward Rate (f) ≈ 5.01%

T

herefore, the implied one-year interest rate starting one year from now is approximately 5.01%.Most Common FAQs

A spot rate is an interest rate for an investment or loan that begins today. A forward rate is an interest rate for an investment or loan that is agreed upon today but begins at a future date. Spot rates are known and directly observable in the market, while forward rates are calculated based on those spot rates.

No, a forward rate is not a forecast or a guarantee. It is an "implied" rate that eliminates arbitrage opportunities between short-term and long-term investments today. Actual future spot rates can and will be different from today's implied forward rate based on new economic information and changing market conditions.

Investors and businesses use forward rates primarily for hedging. For example, a company that knows it will need to borrow money in six months can use a forward rate agreement to lock in a borrowing rate today, protecting itself from a potential rise in interest rates over the next six months.